Among South America’s Largest Portfolio of

Uranium Assets – Argentina & Colombia

Foundational Assets

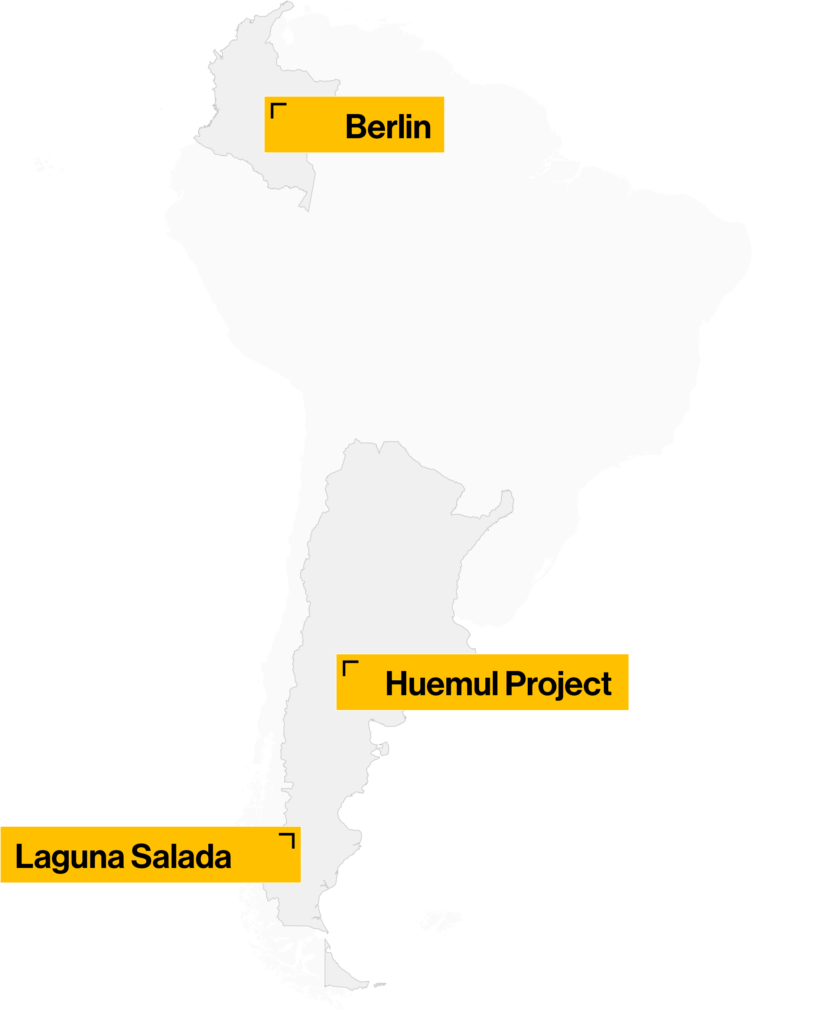

Laguna Salada and Huemul in Argentina, and Berlin in Colombia, anchor a diversified portfolio of large-scale uranium assets

U.S. & Argentina Nuclear Partnership

Assets located in jurisdictions aligned with U.S. nuclear partnership and supported by historical government involvement

Existing Uranium District Infrastructure

Historical geographic uranium production and existing infrastructure reduce development and execution risk

Favorable Jurisdictional Framework

Cornerstone of Argentina’s “Economic Revolution” and Colombian government’s “Green Energy Transition”

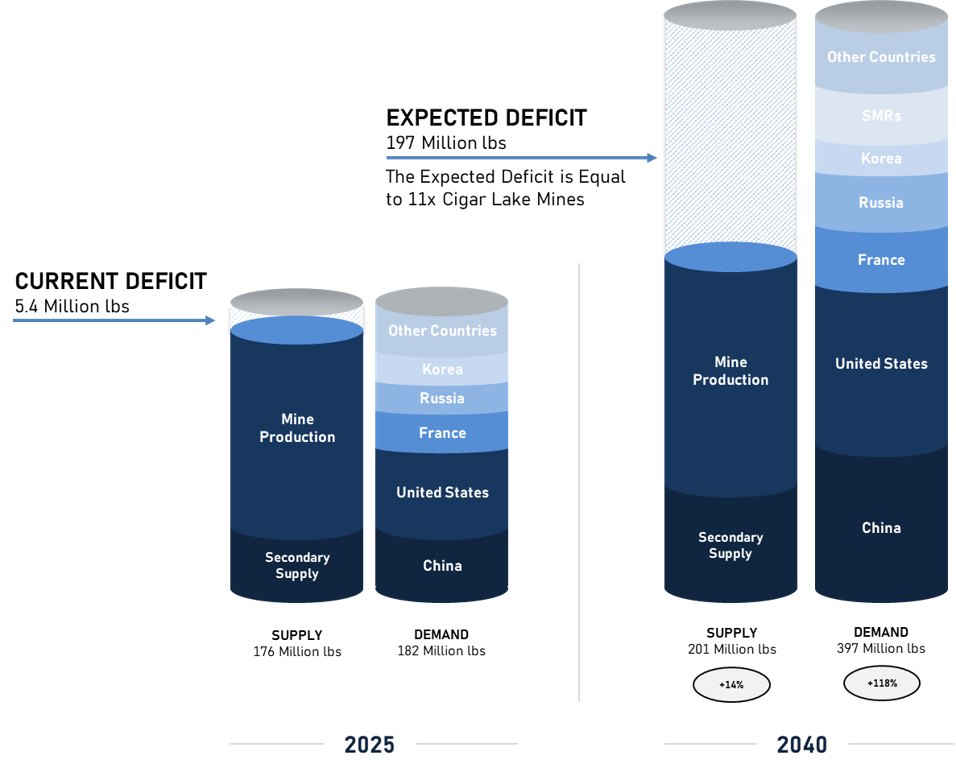

Uranium Imbalance with South America as the Focus

Uranium market in a persistent supply deficit, supporting strong tailwinds

Deficit driven by mine production shortfalls, limited project restarts, underinvestment over the past decade, accelerating SMR (small modular reactors) development, and rising geopolitical tensions

Growing demand for clean, reliable baseload power

Demand growth driven by emerging markets, hyperscaler and AI-driven power needs, and the expansion of SMRs

Regional Energy and Supply Chain Security

“Donroe Doctrine” means South America countries will tacitly or implicitly be under U.S.-influence moving forward

U.S. partnership with South American allies for new supply – Argentina, Colombia, Brazil, Peru

Framework for a United States-Argentina Agreement on Reciprocal Trade

(1) Source: Sprott Asset Management, “The Uranium Opportunity – 2025” infographic, available at sprott.com (2025).

Uranium Supply & Demand

Powering the Future: Advanced Uranium Exploration in South America

Argentina’s Historic and Emerging Opportunities

In Argentina, Jaguar is focused on the Laguna Salada near-surface deposit and further exploration at the historic Huemul Project—the country’s oldest uranium operation. As uranium prices rise and demand for reactor fuel grows, Jaguar is well positioned in Argentina’s uranium reactivation efforts.

Jaguar Uranium’s Berlin Project in Colombia is a high-potential uranium asset, also rich in by-products like vanadium, phosphate, and rare earth elements. With metallurgical testing and strong expansion potential, this project aligns with Colombia’s “Green Energy Transition.”